Union Budget 2026-27 signals a clear shift in India’s industrial strategy—from assembly-led manufacturing, to deeper industrialisation and a stronger mineral ecosystem.

Rare earths are often discussed as ‘resources’, but the binding constraint is not availability—it is the ecosystem that converts geology into usable, bankable industrial inputs. India holds 482.6 million tonnes of identified rare-earth ore resources. For decades, that number remained largely a footnote; the Union Budget 2026–27 is determined to change that.

The announcement of Dedicated Rare Earth Corridors across Odisha, Kerala, Andhra Pradesh, and Tamil Nadu—backed by the ₹7,280 crore Rare Earth Permanent Magnet (REPM) Manufacturing Scheme—represents the most vertically integrated rare earth policy India has articulated to date.

Rare earth value chains do not scale through extraction alone. They scale when the midstream is in place: separation and refining capacity, quality assurance systems, specialised skills, compliant waste management, and reliable logistics. Without this stack, India remains exposed to external supply shocks that show up as higher input costs, delayed project execution, and strategic vulnerability across EVs, renewables, electronics, and defence manufacturing.

The corridor approach, placed alongside the REPM scheme, launched in November 2025, signals a transition from fragmented policy tools to integrated capability creation. The proposal to allow tax deductibility for prospecting and exploration expenditure for select critical minerals further strengthens the front-end by improving discovery economics and investor confidence.

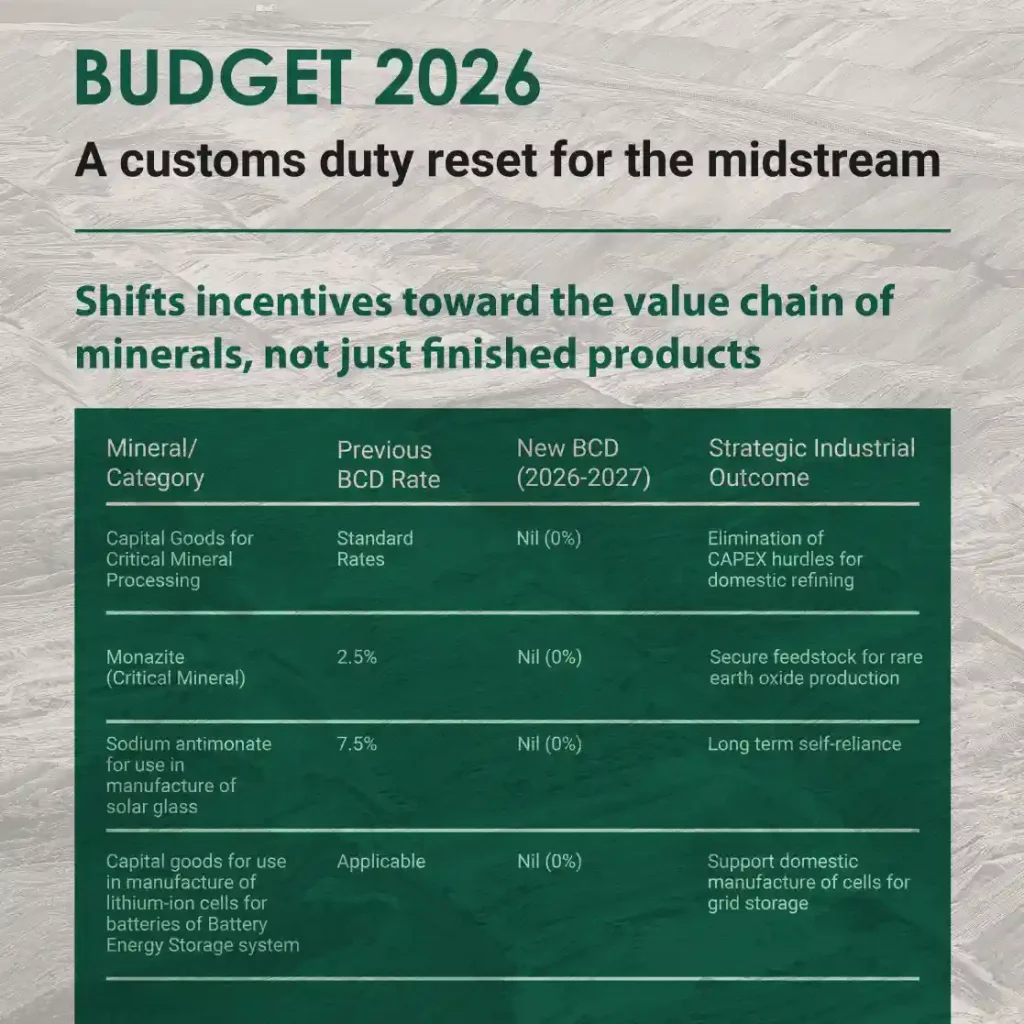

However, the Budget’s architecture goes deeper than corridors and manufacturing schemes. The extension of customs duty exemptions to Lithium-Ion Cells for battery energy storage systems closes a critical gap in India’s clean energy value chain. For the first time, expenditure on prospecting and exploration of critical minerals qualifies for deduction under Section 51—signalling that upstream discovery is no longer an afterthought.

Lastly, the 2026-27 Union Budget’s 20,000 crore allocation for Carbon Capture, Utilization, and Storage (CCUS) is a notable shift in India’s mitigation framework. CCUS is best understood as a bridging capability for hard-to-abate production, not as a substitute for renewables, electrification, or efficiency. The intent also aligns with India’s CCUS roadmap logic: moving from pilots (2025-30) to integration (2030–35) and, if viable, wider deployment (2035–45).

What binds all of this is a shared logic: technological sovereignty requires end-to-end capability, not isolated interventions. From prospecting to processing, from magnets to semiconductors, from manufacturing to decarbonisation—India is not merely participating in the critical materials race. It is architecting its own terms across the entire value chain.

Strengthening Minerals Ecosystem in India: Regulatory and Policy Options

The Expert Roundtable, held on 10 March 2026 in New Delhi, underscored the need to build integrated value-chain capabilities that support industrial growth, resilience, and long-term development.